Last week we talked about the hawkish critiques of U.S. trade with China. They were:

1. that trade with China has strengthened the Chinese Communist state at our expense,

2. that trade deficits strengthen the US dollar and adversely affect US exports,

3. that our loss of manufacturing is a national security issue, and

4. that our trade with China has hollowed out the working class.

I talked at length about the first point: that contrary to the prevailing narrative, the Chinese Communist Party was one of the biggest losers in the globalization of trade. China’s recent success was not centrally planned. It happened only when the CCP stepped aside and allowed its entrepreneurial periphery to do what it has always done well: make and sell. That led to a significant loss of Party legitimacy, forcing it to rebrand as a supplier of infrastructure. Xi Jinping’s authoritarian turn should be viewed as his attempt to pull power back into the middle, because for the last 40 years, it has been in the periphery. Tariffs, as I said, hurt the wrong people, damaging the relatively pro-American, pro-trade periphery rather than the center.

This week we’re going to look at the second point: that our trade deficit with the world—and with China in particular—is akin to the hemorrhaging of blood.

In 2005, Senator Chuck Schumer characterized the growing trade deficit as “a slow bleeding at the wrists economically for the United States.” It’s an image that Democrats like Schumer and MAGA Republicans alike use frequently: defining every dollar we “lose” in trade as like a pint of blood drained from the national body.

Trade deficits and their economic effects are a highly technical affair, and I am not an economic technician. I am more a DIY home tinkerer. But as someone who has worked his whole career within the gears of US-China trade, I’ve seen up-close-and-personal illustrations that bring the abstractions of economic theory to life. Maybe they will help here.

The patron saints of economics—Adam Smith, David Ricardo, and Milton Friedman—as well as most free-trade legends like Paul Krugman, Douglas Irwin, and Jagdish Bhagwati, don’t see the trade deficit as a problem.

A trade deficit means that a country imports more goods and services than it exports. In accounting terms, that sounds bad—like you’re running a loss. But, according to classical free trade theory, that’s just one side of a coin. The other side? Capital inflows. When America runs a trade deficit, it means foreigners are investing in U.S. assets: stocks, bonds, real estate, or even Treasury bills. They’re not taking our money and disappearing into the night. They’re handing it back to us in the form of investment. That’s why the U.S. has had historically low interest rates.

As Paul Krugman has said: “Trade deficits are not a sign of weakness. They’re a sign that foreign investors think your economy is a good bet.”

Mr. Lin’s Trade Deficit

I understand this idea through my friend, Mr. Lin.

He manufactures shoes. For three decades, his family-run factory in Taichung churned out athletic footwear for American brands: first for discount retailers, then, as he improved quality and scale, for bigger names. Year after year, container ships left Kaohsiung loaded with sneakers headed to Long Beach, Oakland, and Houston.

If you were tracking trade flows, you’d say Mr. Lin was part of the problem. From the U.S. point of view, he represented a trade deficit. More stuff came in from Mr. Lin than America sent back to him. His company bought almost nothing from the U.S.—no tractors, no soybeans, no Caterpillar parts. Just raw materials from China, Taiwan, and Vietnam and rubber from Malaysia. Then, all outbound to the USA.

But that’s not the full story.

Mr. Lin didn’t stash his U.S. earnings in offshore accounts or in Beijing real estate. In the early 2000s, he applied for the EB-5 visa program, a federal initiative designed to offer green cards in exchange for direct investment into U.S. businesses that create jobs. The threshold at the time was $500,000 if you invested in a high-unemployment area, or $1 million otherwise.

Mr. Lin bought into a 7-Eleven franchise group in Southern California. Then another. Before long, he owned a string of stores in Riverside and San Bernardino Counties.

And then came the second part of his American plan: education. All three of his children studied in the U.S. The eldest got an engineering degree from Purdue. The second earned an MBA from Michigan. The youngest a JD from UCLA and is now a U.S. citizen.

So, let’s revisit that “trade deficit.”

Yes, Mr. Lin exported more goods to the U.S. than he imported. But then he invested his cash surplus back in U.S. franchises. He created American jobs. He paid U.S. taxes. He educated his children in the U.S. at full international tuition rates, essentially subsidizing American universities.

What Mr. Lin ran with the U.S. was a deficit in goods, but a quite balanced win-win in terms of economic opportunity on aggregate

When you look at it this way, it seems the classical economists have it right.

Surplus of Value, Not Deficit of Parts

Douglas Irwin of Dartmouth reminds us that trade deficits are often just the mirror image of a nation’s strength in attracting global capital and investment. In America’s case, we run trade deficits in goods but surpluses in services, software, finance, and intellectual property, which are the highest rungs of the value ladder.

Richard Baldwin, from IMD Business School in Switzerland, makes the strongest point here, arguing that in today’s world of tightly knit global value chains, trying to judge winners and losers based on trade balances alone is a fool’s errand. What matters more is where you sit in the value chain. And America, for all our handwringing, still sits at the top.

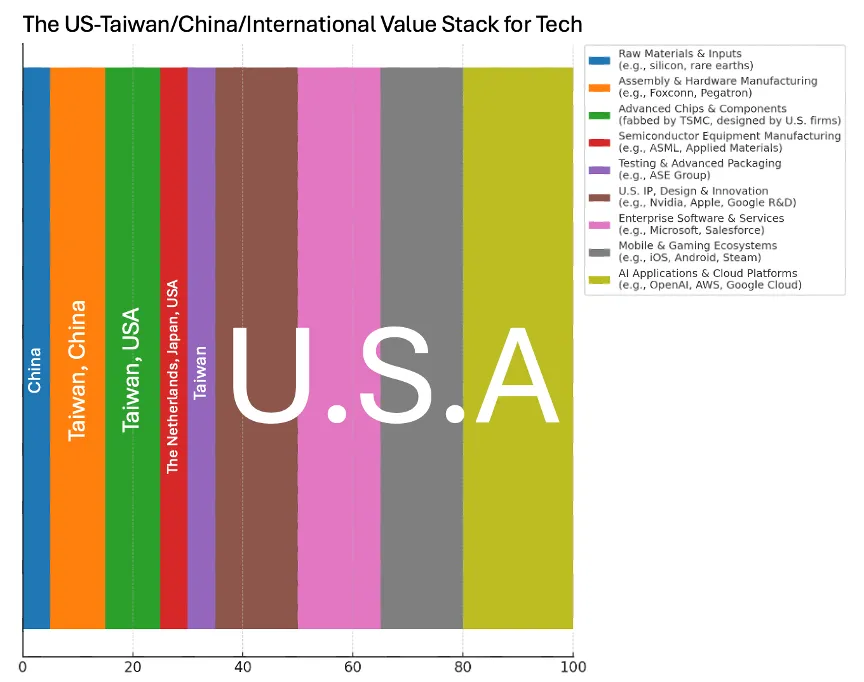

Nowhere is this clearer than in the tech sector.

TSMC, based in Hsinchu, Taiwan, is the world’s most advanced chip foundry. It manufactures over 90% of the globe’s cutting-edge semiconductors, powering everything from iPhones to data centers to AI clusters. Foxconn, headquartered in New Taipei City, assembles the gadgets themselves—iPhones, MacBooks, Xboxes, and Google Nest hubs—all with mind-bending efficiency.

Their shipping manifests are full of silicon, sensors, and screens. These arrive in America in vast containers. If you’re a trade hawk reading the U.S. import ledger, it looks like another story of deficit: Taiwan and China sending goods, America sending dollars. In 2023, the U.S. ran a $40 billion trade deficit just with Taiwan, mostly from electronics and components.

But like Mr. Lin—that’s not the real story. Because what lands on American soil isn’t just parts—it’s potential.

TSMC’s 3nm chip, for instance, goes into Apple’s latest processors. It allows the iPhone to run faster, cooler, and more securely. But the real value doesn’t sit on the chip. It sits on what that chip unlocks: Face ID, real-time rendering, 4K video editing, and AI processing, all delivered through Apple’s iOS ecosystem, now valued at over $3 trillion.

The same goes for Google, whose Pixel phones and AI servers rely on chips fabbed by TSMC. Or NVIDIA, which designs the world’s most powerful GPUs and then has TSMC manufacture them, before selling them into cloud clusters that power ChatGPT, DeepMind, and thousands of AI startups.

The chips and gadgets that come from Taiwan and China are really value levers. They’re the infrastructure for trillion-dollar American software platforms, gaming engines, app stores, streaming empires, and AI breakthroughs.

But Is There Some Bleeding?

For Taiwan—and most of our other trade partners—the classical thinking on trade deficits holds up well. But as we turn our gaze toward China, the picture gets more complicated.

Milton Friedman once said:

“A trade deficit is not a problem in a system of floating exchange rates.”

But that’s just it: China doesn’t have a floating exchange rate. And it doesn’t have a truly open capital account either.

That’s where economist Michael Pettis of Peking University steps in. His work focuses not on trade tariffs or cheating, but on the internal structural distortions within China that inflate its trade surplus and, in turn, the U.S. trade deficit. He doesn’t reject Friedman’s free trade logic, he argues that Friedman’s assumptions break down when the system isn’t free.

According to Pettis, China deliberately suppresses household consumption through policies that keep wages low, restrict the social safety net, and limit profitable savings options. This drives up China’s national savings rate, especially among corporations and the state, and that excess capital must go somewhere. But because Chinese citizens can’t easily invest abroad, it mostly goes into state-controlled banks, which in turn provide ultra-low-interest loans to Chinese industry—including exporters. In Pettis’s words, these are “implicit subsidies” (Pettis, 2013).

This helps China keep exports flowing outward, but distorts global capital flows, and creates a structural imbalance with trade partners like the U.S.

Me, Ms. Chen, and China’s Locked-Up Capital

I’ve felt this imbalance firsthand.

I’ve made several investments into China—factories, joint ventures—and I know what it’s like to try to get your money out. I’m talking about legitimate returns: dividends, repayments, capital gains. You don’t just walk into a bank and wire it home. You need local bank approval, then government approval, and a very clear sense that they’d rather you not move that money out of China at all.

And for Chinese citizens, it’s even tougher.

Take Ms. Chen. She’s a mid-level manager in the Shanghai office of a European multinational. Smart, sharp with numbers, speaks fluent English. She earns well, lives in a nice apartment, and saves about a third of her income. But when it comes to investing those savings, she’s stuck.

She’d love to buy a small flat in Vancouver. Or invest in a U.S. index fund. Or put some cash into her cousin’s startup in Singapore. But she can’t. China’s capital controls make it almost impossible to move large sums overseas. Even sending $50,000 abroad means layers of paperwork and approvals. Go above that, and she risks unwanted scrutiny.

And it’s not like the domestic options are great. The Chinese stock market is volatile and politically sensitive. The real estate market is… well, let’s just say overbuilt. So what does she do? The only thing she can do. She parks her savings in a state-run bank, earning paltry interest. That money then gets recycled into China’s industrial machine—into more steel, more glass, more exports.

Ms. Chen isn’t avoiding the global economy because she doesn’t trust it. She just can’t reach it.

Systemic Imbalance, Not a Morality Tale

Pettis argues that if capital were allowed to flow more freely out of China, more money would chase foreign assets: U.S. goods, services, real estate, and more. The trade imbalance would start to even out, not because we exported more soybeans, but because Chinese consumers could finally become real participants in global consumption.

But that would mean Beijing ceding power to the Periphery. When capital flows outward, the center loses control, and the entrepreneurial periphery gains influence. And we’ve already talked about what Beijing thinks about that.

So the imbalance remains.

That’s why Pettis believes tariffs miss the point. They treat a symptom, not the cause.

Toward a Smarter Negotiation

If Pettis is right—and I think he is—then the U.S.–China trade imbalance isn’t just about Americans over-consuming. It’s about China under-consuming, unnaturally and deliberately.

So what should we do?

Instead of hammering China with blanket tariffs—which often backfire—we should negotiate for structural reforms. We should encourage China to:

- Raise household consumption via higher wages and better social services.

- Liberalize their capital accounts gradually, giving Chinese investors real global options.

- Open up China’s service sector to foreigners—education, finance, healthcare—where the U.S. leads.

- Redirect Chinese excess capital into third-country infrastructure (a Belt & Road alternative).

If China wants continued access to American consumers, then a fair ask is that they gradually build a system that empowers the millions of Ms. Chens. Will they resist? Absolutely. A financially empowered citizenry is a threat to central control.

But this is precisely why the U.S. needs a smart, system-level strategy—not just punitive duties.

Tariffs smash the negotiating table, ensuring nothing changes.

I’m afraid The Deal needs to be way more artful than that.